Contract awards on major regeneration and infrastructure projects have seen ‘hotspot’ pockets of construction emerge across Great Britain as investment in housebuilding, infrastructure and commercial shifts away from London and the South East.

The ‘Regional Construction Hotspots in Great Britain 2017’ report from industry analysts Barbour ABI and the Construction Products Association, highlights the levels of construction contract values awarded in 2016 across all regions of Great Britain. London saw a decrease of 15 per cent compared to 2015, down to £13.1 billion on the year.

Looking at the London districts from a national perspective, only two London regions made it into the top ten for overall construction value in 2016 – Tower Hamlets and Camden & City of London, fourth and eighth respectively, boosted by projects such as the £300 million Chrisp Street development in Poplar and the £500 million 22-24 Bishopsgate tower in the City (formerly the Pinnacle).

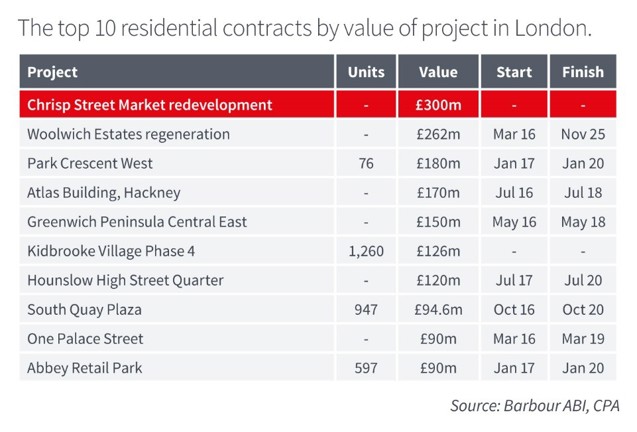

For residential construction (see Figure 1.1), in contrast to other regions in Great Britain that experienced a fall in contract value in 2016, London’s annual total held steady at £5.5 billion, with developments such as Greenwich Council’s £262 million Woolwich Estates regeneration and the Atlas Building in Hackney with a contract value of £170 million.

(Figure 1.1)

Looking at the commercial sector in London, contract awards totalled £3.4 billion in 2016, broadly unchanged from the 2015 value. Key commercial projects commissioned in the capital in 2016 include four worth over £250 million: 22-24 Bishopsgate, Ten Bank Street in Canary Wharf, Bechtel House in Hammersmith and Building S4 at the Olympic Promenade in Stratford.

Infrastructure projects however totalled £1.5 billion in 2016, a 50.5% decrease from 2015, but that does put the sector in line with the long-term average. Major contracts awarded include £350 million for HS2, £170 million for upgrades to baggage facilities at Heathrow and £150 million for the Garden Bridge, which is now in doubt after official funding was scrapped.

Hotspots

In past years, London frequently dominated the ‘hotspot’ pockets of construction activity, however the report for 2016 indicates a spread right across Great Britain, with London only holding six of the sixty-one hotspots.

London hotspots for commercial activity were Bromley, Kensington & Chelsea and Hammersmith & Fulham, Hackney and Newham. Barking & Dagenham and Havering were the main hotspots of activity for infrastructure, due to utilities projects including a £70 million energy-from-waste plant and a £30 million anaerobic digestion plant.

Coldspots

London was the sole region where there were no residential coldspots, with contract awards for large developments keeping values relatively unchanged from 2014 and 2015. There were also no infrastructure coldspots across the London districts.

Two London districts – Brent, Camden & the City of London - saw commercial activity cool to below long-term averages in 2016, but this was the joint lowest number of regional coldspots in Great Britain, tying with the North East.

Commenting on the figures, Michael Dall, Lead Economist at Barbour ABI, said: “After a fruitful year for construction in 2015, especially in the capital, it was always going to be challenging replicating similar figures, particularly with the uncertainty of Brexit falling in the midst of 2016. However, housebuilding once again proved to hold strong and ‘prop up’ construction with a number of major developments commissioned across the city, as investors and housebuilders continue to see the value in developing residential property in London.”

Rebecca Larkin, Senior Economist at the Construction Products Association commented; “With residential and commercial contracts having remained at high values, the sharp decrease in infrastructure contract awards in London during 2016 was disappointing. It is, however, softened by the fact that values simply dropped back to relatively normal levels after an impressive 2015. That means construction output over the next few years will be buoyed by work on previous hotspots – the Thames Tideway Tunnel and the Gospel Oak-Barking Overground extension for example – with new projects awarded contracts in 2016 adding to the pipeline of activity.”

View the Regional Hotspots in Great Britain 2017 report here.

-ENDS-

Notes to editors:

Press enquiries to:

Jonathan Touhey at Barbour ABI

Tel: 0151 353 3605

Mobile: 07976 837339

E-mail: jonathan.touhey@barbour-abi.com

Emma Salmon, CPA Marketing and Communications Executive

Tel: 020 7323 3770

E-mail: emma.salmon@constructionproducts.org.uk

About Barbour ABI:

Barbour ABI is a leading provider of construction intelligence services. With a team of in-house research specialists and a dedicated economics team, it provides commercially relevant insight and unique analysis of trends and developments within the building and construction industry.

Barbour ABI is the chosen provider of Construction New Orders estimates data to the Office for National Statistics, provider of the Government’s Construction and Infrastructure Pipeline and provides the planning application and development data to the Department for Communities and Local Government. Barbour ABI also provides data for independent organisations, such as the Construction Products Association.

Barbour ABI is part of global events-led marketing services and communications company, UBM, and is headquartered in Cheshire Oaks, Cheshire.

For more information, go to www.barbour-abi.com or follow on Twitter @BarbourABI for all the latest construction data news.

About the Construction Products Association:

The Construction Products Association represents the UK's manufacturers and distributors of construction products and materials. We are committed to raising the profile of our industry and members' businesses, helping grow the market and reducing regulatory risk. The sector directly provides jobs for 300,000 people across 22,000 companies and has an annual turnover of more than £55 billion. The CPA is the leading voice to promote and campaign for this vital UK industry.

The CPA produces a range of economic reports including the quarterly Construction Industry Forecasts, Construction Trade Surveys and the State of Trade Surveys. All are available to members or subscribers via our website.

Much of the CPA's work is focused on serving as the first point of contact for politicians and policy makers requiring advice and information about matters that affect construction products or the wider construction industry. This includes understanding the need for investment into manufacturing or the built environment, new housing and energy-saving retrofitting of the existing housing stock; helping to develop effective, UK and EU legislation, regulations and product standards; and promoting the role of manufacturers in delivering a resource efficient built environment.

Follow the Construction Products Association on Twitter: twitter.com/CPA_Tweets.